Goa is abuzz with excitement as vintage bike and car owners, users, collectors and fans are decking […]

Old is Gold

October 4, 2016

ONE of the unique grass root systems in the country is the co-operative movement. India being a rural country, which until lately had little access to the banking system, cooperative credit societies play a vital role in channelizing credit to agriculture and small businesses. Credit cooperative societies flourish in our country and are one of the enduring pillars of financial architecture, especially in areas where our banking system is yet to develop. Most of these cooperative structures in our country are controlled by our political parties, since these cooperative fora are the training ground for grass root level politicians. The political class continue to dominate these organizations and over a period of time many of financial cooperatives have become inoperative or defunct. Let’s look at the Goan scene

During the Portuguese era, Goa had a system of land holding an institution called “communidades.” These village level groups were in charge of the communal lands, grazing grounds and community property. Out of the income they generated, the profits were distributed by way of “zhon” at the end of the accounting period. Unfortunately after 1961, this institution of the communidades fell into disuse, with no adequate supervision by the Indian state.

AGRICULTURE, DYING SECTOR

SUBSEQUENTLY, when Goa became part of the Union, the cooperative movement gathered momentum in the ‘60’s in the with the aim of uplifting the weaker sections of society. Cooperative societies initially focussed on agriculture and rural credit and coupled with economic growth expanded into housing, consumer goods, dairy farming fishing and urban credit. In order to regulate this sector, the Goa Cooperative Societies Act 2001, was enacted and followed by Rules in 2003. The Registrar of Cooperative Societies functions from Panjim. As on date Goa has 5,433 registered societies with over 1.57 million members. 4315 of these societies are function while 1032 societies are non-functional of which 86 are under liquidation. A look at the data tells you that a quarter of the societies are non-function an indication of the malaise that exists in the cooperative sector. Over the years, Goa has not established any new primary agricultural credit societies. This is probably due to the fact that in Goa, agriculture is a dying sector. Travel across the length of the state and what was once verdant farmland has become barren plots, waiting for the real estate sector to buy these properties. Among the many reasons for the decay of agriculture cooperatives is the plot size, the lack of labour and poor renumeration from land.

Goa has around 2,500 credit cooperative societies. However many of these are stressed facing both regulatory and audit defaults. Sadly most cooperative societies fact loan recovery issues leading to financial instability. Many of these societies have weak management and lack professional oversight and most of all political interference in their day to day functioning. Unfortunately several politicians or their close associates occupy positions of authority in cooperative credit societies, influencing influencing both the amount, tenor and coupon rate of loans being distributed. Further even when the assets become bad, there is little enforcement of dues, since many of these loans are approved on the basis of political patronage. In 2024, the Fatorda MLA had highlighted the fact that 18 cooperative credit societies that have cheated its depositors of around 20 crore.

Take the case of the Mashel Mahila Cooperative Credit Society. This society had around 509, depositors mostly women who contributed their life savings into this fund. In 2024, there was a fraud of Rs18 crore. The government instituted a probe into the fraud, inquiring an inquiry officer to recover the money. Till date, the enquiry is still pending. In a reply in the Goa assembly, the government has in the assembly admitted that with the around 20 crores has been lost by depositors since 2016.

I remember, during my stint in Goa as Commissioner Income tax, one complaint related to a “ponzi scheme” where depositors formed a financial cooperative where they were assured of 24 percent interest together with lavish gifts. These original depositors were in turn required to being in other depositors to continue obtaining this high rate of interest on their original deposits, that they never got back. Sure enough the scheme failed and several depositors lost several lakhs in the scheme. Many of these smaller scams do not even surface, the depositors just write off their losses!

COOPERATIVE BANKS

GOA is also a state that has several active cooperative banks. At the apex level is the Goa State Cooperative Bank Ltd (GSCB) established in 1963, in serves as the apex institution in Goa’s cooperative credit structure. It functions as the state cooperative bank, supervising and supporting the primary agricultural cooperative credit society across the State. Further it operates 54 branches across the state. GSCB over the years has been grappling with losses and low profitability.

However, the Goa State Cooperative Bank is now a well-managed bank and continues to function as the apex bank in the State. This is not the case with many of the other cooperative banks.

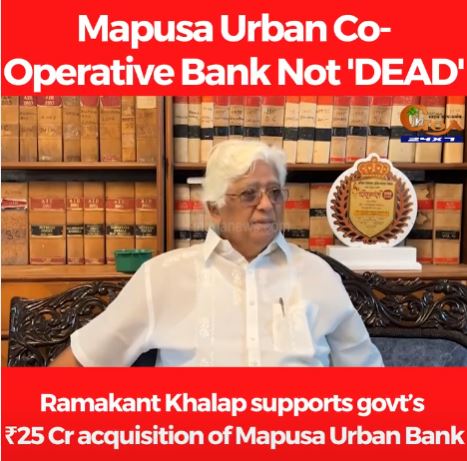

Most of these are helmed by politicians and over the decades have gone to seed. The Mapusa Urban Cooperative Bank had its banking licence cancelled in September 2025, after repeated merger proposals failed. This bank was originally founded in 1965, by a group of 27 big town merchants, industrialists and agriculturists, who believed that having a cooperative bank in North Goa would help to develop business. With the Khalap family at its helm, the bank grew rapidly, obtaining schedule status from the RBI and multi state status in 1998. However, over the decades with bad loans, poor assets, and with growing defaults of its loans, the bank is today under liquidation with an administrator at its helm.

Similar is the case with the Madgaum Urban Cooperative Bank, founded in 1972 to serve the needs of small savers and traders in South Goa. This bank is now in liquidation and an administrator has been appointed to protect the interest of the depositors. One of the many reasons why Madgaum Urban Cooperative Bank went into liquidation was the lack of inadequate capital to continue its operations. Its poor assets book, and its failure to meet the regulatory compliance of the RBI.

However, not all Goan cooperative banks are sick. The Bicholim Urban Cooperative Bank, with its headquarters in Bicholim, the Women Cooperative Bank, the Goa Urban Cooperative Bank, both headquartered in Panjim, continue to function The RBI continues to monitor the health of these banks. A year ago, in the case of Citizen Bank, on an assessment of its financial instability, the RBI has merged this cooperative Bank with Thane Jan Sahakari Bank

With urbanization, Goa has several housing cooperative societies. These societies continue to maintain apartment housing buildings. Several of these function adequately since many of their members are aware of the various cooperative provisions. However, in many of these societies, there are irregularities with regard to society dues, and regulatory issues in terms of reporting to the Registrar of Cooperative Society.

POOR GOVERNANCE

WHILE the cooperative sector has grown in Goa, there is need of an awareness of the regulatory and compliance issues in many of these cooperative bodies. Unfortunately, governance is poor and the complicity of the political class in many of these bodies, ensures that measures required to strengthen the regulatory framework is lacking. Unless there is a strong regulatory framework that will ensure compliance, the political class will continue to exploit these cooperatives for their own advantage!

LETTERS TO THE EDITOR FOR ISSUE DATED APRIL 04, 2026

LETTERS TO THE EDITOR FOR ISSUE DATED APRIL 04, 2026 REAL ESTATE BARONS OF GOA!

REAL ESTATE BARONS OF GOA! THE SLOW VANISHING OF GOA’S GOLDEN BEACHES! By Raaisa Lemos Vaz

THE SLOW VANISHING OF GOA’S GOLDEN BEACHES! By Raaisa Lemos Vaz WHO IS EXTRACTING GOA’S GROUND WATER? By Supriya Vohra

WHO IS EXTRACTING GOA’S GROUND WATER? By Supriya Vohra PLANNING FOR RETIREMENT THE GOAN WAY! By Arvind Pinto

PLANNING FOR RETIREMENT THE GOAN WAY! By Arvind Pinto WHEN `HOLY WEEK’ COMES LONG

WHEN `HOLY WEEK’ COMES LONG HPV Vaccine: PROTECTING INDIA’S DAUGHTERS FROM CERVICAL CANCER!By Dr Amit Dias, MD

HPV Vaccine: PROTECTING INDIA’S DAUGHTERS FROM CERVICAL CANCER!By Dr Amit Dias, MD NO MORE PROTESTS AT AZAD MAIDAN?

NO MORE PROTESTS AT AZAD MAIDAN? CURCHOREM SEX SCANDAL: Will the police really take action?By Olav Albuquerque

CURCHOREM SEX SCANDAL: Will the police really take action?By Olav Albuquerque WEEKEND UPDATESLETTER TO THE EDITOR FOR THE ISSUE DATED MARCH 28, 2026

WEEKEND UPDATESLETTER TO THE EDITOR FOR THE ISSUE DATED MARCH 28, 2026 GOA’S GILDED HIGH RISE SLUMS!By Raaisa Lemos Vaz

GOA’S GILDED HIGH RISE SLUMS!By Raaisa Lemos Vaz DIRTY TOWERS OF GOA!

DIRTY TOWERS OF GOA! UNCLEAN WATER, CARRIER OF DISEASE! By Dr Amit Dias, MD

UNCLEAN WATER, CARRIER OF DISEASE! By Dr Amit Dias, MD LOOKING BACK AT GOA IN 60S! By Arvind Pinto

LOOKING BACK AT GOA IN 60S! By Arvind Pinto

Goa is abuzz with excitement as vintage bike and car owners, users, collectors and fans are decking […]