Goa is abuzz with excitement as vintage bike and car owners, users, collectors and fans are decking […]

Old is Gold

October 4, 2016

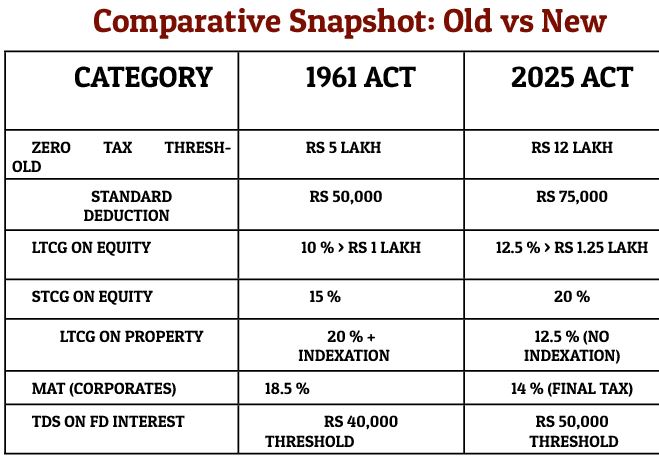

THE new income tax act of 2025, which came into effect from April 1, 2025 till April 1, 2026 has not made the expected headlines in the media, but it has certainly overhauled this vital fiscal legislation both for the tax-payer and gatherer. While for many of us who have been schooled in tax with the 1961 Act, the new Code with its revised numbering of sections may at first glance appear puzzling; but on a deeper reading indicates that much of the older sections have been reworked into a more compact and well- meaning digital design. The Income Tax Act, 2025 contains 536 sections and 16 schedules compared to the 819 sections and 14 schedules of the 1961 Act.

BIT OF HISTORY

HISTORICALLY, all political regimes in India levied tax on income. The British Income Tax Act 1922, brought about a codification of differing legislations on income- tax for those residing within the British provinces; while the princely states had their own version of income tax. At that period direct tax was a marginal tax with limited number of payers and scanty compliance. When the Income Tax Act of 1961 came into force, India was a newly independent economy still defining its fiscal identity. The 1961 Act saw amendments made to it each year during the budget presentation. These amendments were necessitated to expand its scope, to cater to judicial interpretation or ease difficulties in implementation. Sixty four years later, the Income Tax Act, 2025 marks a generational shift—an attempt to align taxation with the realities of a digital, mobile, and globally integrated India. This piece of legislation is a statement that India has come of age, in direct taxation.

This reform is not merely a rate revision; it is a conceptual overhaul. It replaces archaic terminology, simplifies compliance, and re centres the taxpayer in the system. The Act’s architects describe it as “a move from interpretation to intuition”—a framework that ordinary citizens can understand without professional mediation. This would indeed be pleasing to many, who were unable to decipher the legalese of the 1961 statute.

CORE STRUCTURAL CHANGE, `TAX YEAR’ REVOLUTION

UNDER the old regime, taxpayers had to navigate between two overlapping time frames: the Previous Year (when income was earned) and the Assessment Year (when income was assessed ). This duality created confusion, especially for small businesses and salaried individuals who struggled to reconcile fiscal years with the assessment calendars.

The new act abolishes this duality. Income earned between April 1 and March 31 is taxed in the same tax year. For example: Income earned from April 2026 to March 2027 is taxed in tax year 2026 27. Accordingly, returns, advance tax payments, and tax deducted at source certificates all reference this same year. This change is more than linguistic — it eliminates the one year lag between earning and assessment, aligning India with global practice. For professionals and institutions, it simplifies accounting cycles; for policymakers, it improves real time fiscal data. Now with a single concept namely “tax year” makes it easy for everybody to understand, what is their income and how much tax is payable thereon. It also puts paid to the tax planning that clever lawyers would resort to when there is a spurt of income in any given year.

RAISING THE FLOOR: A FAIRER THRESHOLD

THE zero tax threshold has been raised from Rs5 lakh to Rs12 lakh, accompanied by an enhanced rebate of Rs60,000. This single measure pulls nearly 40 million low income taxpayers out of the tax net, reflecting a deliberate shift toward progressive taxation. The standard deduction for salaried individuals rises to Rs75,000, acknowledging inflation and the cost of living. Pensioners and senior citizens benefit from a higher deduction on interest income — Rs50,000 per bank instead of Rs40,000 — reducing compliance friction for those with multiple accounts. Hopefully the raising of limits will be of benefit to several marginal taxpayers, especially senior citizens.

The pattern is clear: lower rates, broader base, simpler computation. The government’s intent is to make compliance intuitive rather than interpretive. Hopefully the government’s liberality and trust on its citizen’s will increase tax compliance.

COMPLIANCE SIMPLIFIED: FORM 130 & DIGITAL INTEGRATION

THE Form 16 era ends. In its place comes Form 130, a unified, portal generated certificate with three parts —A (TDS summary), B (income details), and C (deductions and exemptions). Employers will no longer issue manual certificates; all data would flow through the Income Tax Portal 2.0, integrated with PAN, Aadhaar, and GST data. This would be of use to the tax-payer, who would have income in a single unified portal.

This digital consolidation serves two purposes: a) Transparency — reducing manipulation of salary slips and deductions. b)Automation — enabling pre filled returns and instant verification. For banks and financial institutions, this means CBS systems must update their tax modules to reflect Tax Year terminology and Form 130 integration. For lawyers and accountants, it means re training staff and revising templates.

SECTION RE-NUMBERING: LEGAL DRAFTSMAN CHALLENGE

EVERY section of the 1961 Act has been renumbered. One of the sections most remember is Section 80C where one could claim deductions for savings, such as provident fund, LIC, etc. This section is now renumbered Section 123. We knew Section 87A was for rebates, under the new Act it has been renumbered Section 156. Section 10 (exempt incomes) becomes Section 11, now divided into schedules. This renumbering is not cosmetic — it reflects a logical grouping of provisions by taxpayer category rather than by historical sequence. However, it poses a challenge for legal practitioners: contracts, judgments, and precedents citing old sections must be cross mapped. The government has released a conversion schedule, but transitional litigation will be inevitable.

CAPITAL GAINS: RATIONALISATION & REALITY

OVER the years, different acts have had a different regime on the taxation of capital gains. This act has attempted a rationalisation of the provisions. Long term capital gains on shares will be 12.5 % above Rs1.25 lakh. The concept of indexation has been done away with. In case of property LTCG at the rate of 12.5 % without indexation, replacing the 20 % indexed regime. In the case of short term capital gains 20 % flat for equities and property. The rationale is clarity —indexation benefits were complex and often misused. The trade off is that long term investors lose inflation adjustment, but gain predictability. For real estate markets, this could encourage faster turnover and discourage speculative holding. The concept of indexation was brought about to make adjustment for inflation over the years. However this concept has led to both litigation and tax disputes. It would be left in the coming years to be seen whether the government would need to revisit the concept of indexation.

CORPORATE TAXATION: MAT & BUY BACK REFORMS

THE Minimum Alternate Tax (MAT) the tax that companies pay, where the deductions that can be claimed are greater than the income , now drops to 14 % from the earlier 15% , but crucially, it becomes a final tax — no more MAT credit accumulation. This simplifies accounting for companies with fluctuating profits. The Buyback Tax when companies decide to buy back shares shifts from company level taxation to shareholder level capital gains. This aligns India with OECD norms and removes the distortion that penalised companies for returning capital to investors.

TRANSITIONAL DUAL COMPLIANCE: FY 2026 27

THE transition year is unique. Taxpayers must: File returns for AY 2026 27 under the old Act (income earned Apr 2025–Mar 2026).Pay advance tax for Tax Year 2026 27 under the new Act (income earned Apr 2026–Mar 2027).

This overlap creates a dual compliance burden for one year. The government has issued circulars allowing leniency in penalties and interest for genuine errors during this phase. From FY 2027 28 onward, the system stabilises. In a transitional year there is always an amount of uncertainty. Many of these unresolved issues reach the Court. However, if these issues can be resolved by issuing guidelines, several of these problems could be resolved at the executive level.

GLOBAL ALIGHNMENT & DIGITAL GOVERNANCE

THE reform mirrors global trends: United Kingdom and Australia use single year taxation. Singapore and UAE have digital pre filled returns. The Organisation for Economic Co-operation and Development (OECD), Base Erosion and Profit Shifting (BEPS) framework encourages transparency and real time reporting. Hopefully the new Indian tax regime will ensure that India is able to tax its legitimate share of income from transnational transactions.

India’s move to a Tax Year and portal based compliance positions it within this global ecosystem. It also enables AI driven analytics for revenue forecasting and fraud detection—an area where the Central Board of Direct Taxes (CBDT) is investing heavily.

POLICY PHILOSOPHY: FROM ENFORCEMENT TO EMPOWERMENT

THE 1961 Act was designed for enforcement — its language was adversarial, its structure punitive. The 2025 Act pivots to empowerment. It assumes voluntary compliance and builds trust through clarity. Three philosophical shifts stand out: a) Language Simplification — legalese replaced by plain English, this will enable the common man to understand the provisions and would help small tax payers to comply without the aid of a professional. B) Predictability —fewer discretionary powers for assessing officers. C) Digital Accountability — every transaction traceable, every deduction verifiable. The changes reflects a broader trend in governance: citizen centric design. The taxpayer is no longer a suspect but a participant in nation building. The changes have also several implications for professionals; for lawyers and chartered accountants the new sections would require cross referencing between old and new sections especially in drafting contracts and pleadings. Transitional disputes will arise over interpretation—especially in capital gains and TDS provisions. The Act’s plain language drafting may reduce litigation over ambiguity but increase it over transition. Most importantly for bankers especially working with CBS and compliance systems must adopt to the new Tax Year terminology. The tax deduction at source modules must integrate with Form 130 and new thresholds. MAT and buyback changes would necessarily affect corporate clients’ tax planning.

Like most institutions in India, the tax department has gone both digital as also faceless. Gone are the days, when assessee had to wait outside an officers’ chamber to settle a tax issue, or complain about non- receipt of a refund. This new Act 1925 with its simplicity and compact character will hopefully help in understanding of the concept of tax payable on income, make it easier for multi-national corporates to do business in India, and enhance the capability of the cadre of the Indian Revenue Service to make it on par with its counterparts in the developed world.

CONGRESS REBELS PACIFIED!

CONGRESS REBELS PACIFIED! GOA’S DAMS FACE SLOW MONSOONS!By Raaisa Lemos Vaz

GOA’S DAMS FACE SLOW MONSOONS!By Raaisa Lemos Vaz ALZHEIMER’S EMERGING AS A GROWING CONCERN IN AGEING GOA…By Dr Parul Dubey

ALZHEIMER’S EMERGING AS A GROWING CONCERN IN AGEING GOA…By Dr Parul Dubey CAN HOSPITALS HOLD PATIENTS “HOSTAGE” OVER UNPAID BILLS?By Keral Mehta, Yati Sharma

CAN HOSPITALS HOLD PATIENTS “HOSTAGE” OVER UNPAID BILLS?By Keral Mehta, Yati Sharma `THE LITTLE PRINCE’ IN MANGLISH…

`THE LITTLE PRINCE’ IN MANGLISH… THE CHARMS OF HORCHATA… An Iberian sherbat! By Tara Narayan

THE CHARMS OF HORCHATA… An Iberian sherbat! By Tara Narayan DATTA NAIK TOPPLES SHENOI GOEMBAB FROM PEDESTAL!

DATTA NAIK TOPPLES SHENOI GOEMBAB FROM PEDESTAL! CONTROVERSY ERUPTS OVER MHADEI RIVER DIVERSION Goa clashes with Karnataka again! By Dr Olav & Deborah Albuquerque

CONTROVERSY ERUPTS OVER MHADEI RIVER DIVERSION Goa clashes with Karnataka again! By Dr Olav & Deborah Albuquerque WEEKEND UPDATES

WEEKEND UPDATES LETTER TO THE EDITOR FOR THE ISSUE DATED JULY 04, 2026

LETTER TO THE EDITOR FOR THE ISSUE DATED JULY 04, 2026 BATTLE WON BUT WAR REMAINS!

BATTLE WON BUT WAR REMAINS! BITCOIN FOR BEGINNERS! By Arvind Pinto

BITCOIN FOR BEGINNERS! By Arvind Pinto POLYMER NOTES, CLEANER CASH, NOT CURE-ALL!By Satish Singh

POLYMER NOTES, CLEANER CASH, NOT CURE-ALL!By Satish Singh WHEN IT COMES TO BIRTHDAY CAKES I STILL WANT TO ORDER `BOL SANS RIVAL’…By Tara Narayan

WHEN IT COMES TO BIRTHDAY CAKES I STILL WANT TO ORDER `BOL SANS RIVAL’…By Tara Narayan GOA’S 56-VILLAGE U-TURN EXPOSES DEEPER CRISIS OF TRUST! By Dr Olav & Deborah Albuquerque

GOA’S 56-VILLAGE U-TURN EXPOSES DEEPER CRISIS OF TRUST! By Dr Olav & Deborah Albuquerque

Goa is abuzz with excitement as vintage bike and car owners, users, collectors and fans are decking […]