Goa is abuzz with excitement as vintage bike and car owners, users, collectors and fans are decking […]

Old is Gold

October 4, 2016

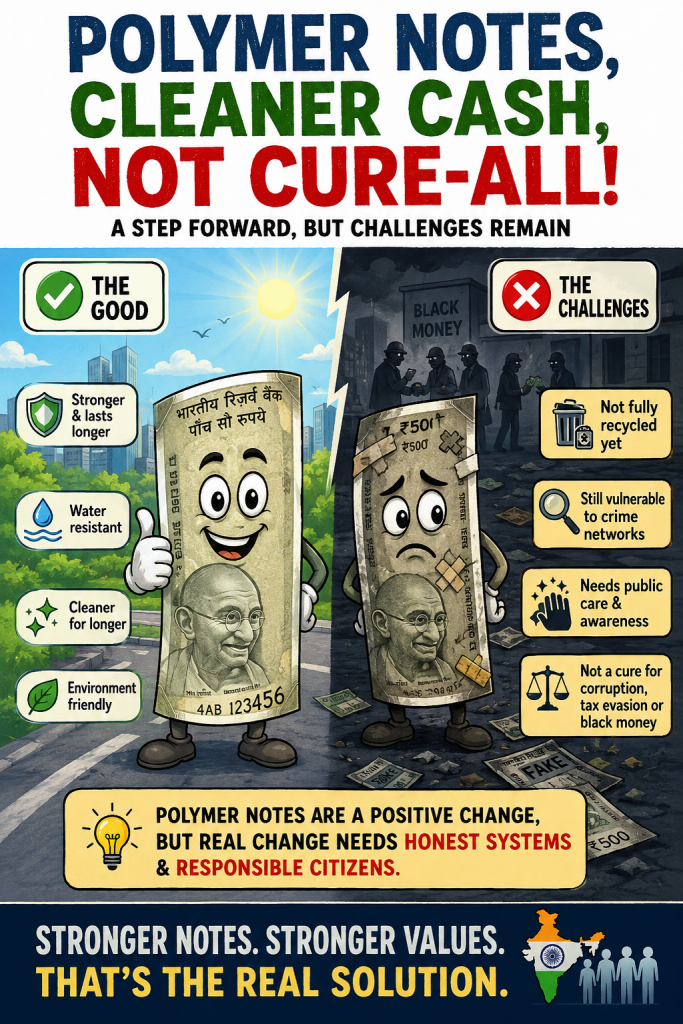

THE debate on polymer, or plastic, banknotes is not new to India. Yet, with the Reserve Bank of India once again examining the possibility, an old question has acquired fresh relevance in the larger discourse on currency management. The issue is not merely whether banknotes should be made of paper or plastic. The real question is whether polymer notes are feasible in a country as vast, diverse, cash-intensive, and climatically challenging as India; who would benefit from them, who might face inconvenience, and whether they can meaningfully address problems such as black money, corruption, hawala transactions, or terror financing.

At the outset, it is important to clarify that India’s existing banknotes are not printed on ordinary paper. They are printed on a specialised cotton-based banknote paper. Polymer notes, by contrast, are printed on a special plastic substrate. Countries such as Australia, Canada, the United Kingdom, New Zealand and a few others have adopted them. Their experience suggests that polymer notes are generally more durable, more resistant to moisture and dirt, and can accommodate stronger security features against counterfeiting.

For India, the first argument in favour of polymer notes lies in the climate. In many parts of the country, humidity, rain, sweat, dust, heat and high cash turnover, shorten the life of banknotes. In small shops, mandis, bus stands, railway stations, rural markets and fairs, notes pass from hand to hand at extraordinary speed. In such conditions, the durability of polymer notes can be a significant advantage. They do not tear easily, are less vulnerable to water damage, and remain relatively clean for longer. This could reduce the cost of withdrawing, sorting, replacing and destroying soiled or mutilated notes.

ENORMOUS TASK

BUT feasibility has another side. India’s currency system is enormous. Bank branches, currency chests, ATMs, cash vans, note-sorting machines, vending machines and cash-processing centres would all have to be calibrated to the characteristics of polymer notes. If the thickness, friction, flexibility, or machine-readable features of the notes change, ATMs and sorting machines may require additional adjustments and expenditures. Shopkeepers, banks and the public would also need to be educated about identifying and using the new notes. Therefore, the question of polymer notes is not merely a printing issue; it is a question of reconfiguring the entire cash ecosystem.

The issue of cost is not straightforward either. The initial printing cost of a polymer note may be higher than that of a cotton-based note because the substrate and security technology are more expensive. However, if a polymer note lasts two to three times longer, its annualised cost over its life cycle may be lower. In other words, polymer notes may be costlier at the beginning, but cheaper over time.

Before taking a final decision, India would need to assess which denomination offers the highest benefit. It may be prudent to begin with lower-value or high-circulation denominations so that durability, machine acceptability and public convenience can be tested under Indian conditions.

The impact on the Indian economy would be more administrative and operational than macroeconomic. Polymer notes would not directly affect GDP or inflation. Their influence would be felt in currency management, counterfeit prevention, note quality and the efficiency of cash circulation. If notes last longer, the replacement cost for the Reserve Bank of India and commercial banks may decline. Cleaner and more durable notes would improve the quality of cash in circulation. This could also help small traders and rural consumers, as disputes over torn, dirty or sticky notes would reduce.

Expectations, however, must remain realistic regarding black money and corruption. Polymer notes may be harder to counterfeit, but they cannot eliminate black money. Black money is not born out of the material of a banknote; it arises from opacity in transactions, benami assets, cash-based payments, tax evasion, political financing and weak enforcement. If the economy remains substantially cash-driven, replacing cotton-based notes with polymer notes will not alter the underlying character of illicit wealth. Corruption, too, cannot be curbed merely by changing the texture of currency. It requires institutional accountability, digital trails, tax discipline, asset disclosure and credible punitive action.

That said, polymer notes can make life more difficult for counterfeiters. Features such as transparent windows, holograms, colour-shifting ink, micro-printing and machine-readable security elements can raise the technological barrier. In India, fake Indian currency notes have not merely been an economic concern; they have also had national security implications. If high-security polymer notes enter circulation, they may put some pressure on cross-border counterfeit networks, hawala channels and terror-financing mechanisms. Yet it would be misleading to assume that polymer notes alone can end hawala or terrorism. Such networks often shift to alternative routes—gold, crypto-assets, trade-based money laundering, over-invoicing, under-invoicing and shell companies. Polymer notes, therefore, can be one instrument in a wider security strategy, not the strategy itself.

For banks, the impact would be mixed. On the positive side, fewer torn or soiled notes could reduce pressure on branches to exchange notes. Currency chests may have to sort fewer unfit notes and remit fewer such notes to the Reserve Bank. The overall quality of cash handling could improve. However, in the initial phase, banks would have to invest in machines, ATMs, cash-counting devices, note-sorting systems, and staff training. Existing methods of detecting counterfeit notes would change. Branches would have to explain to customers how to identify genuine polymer notes and what would happen to existing notes. If the transition plan is unclear, rumours may spread, as often happens in currency-related matters.

ADVANTAGES/DISADVANTAGES

FOR everyday use, polymer notes offer clear advantages but also some inconveniences. They do not get damaged by water easily, do not deteriorate quickly due to sweat, and remain cleaner for longer. However, some countries have reported that new polymer notes can initially feel slippery, may stick together while counting, and may be less convenient to fold. In India, where many people fold notes and keep them in wallets, pockets, cash boxes, places of worship or informal rural account books, usage habits must also be studied. For visually impaired citizens, tactile identification, note size and touch-based markers would require special attention.

The environmental argument is also more complex than it appears. Since polymer notes are made of plastic, they may seem environmentally unfriendly at first glance. But if they last much longer and can be recycled through a controlled process, their total environmental cost may be lower. On the other hand, if the recycling chain is weak, disposal of old polymer notes may create a new problem. Before moving forward, India should conduct a full environmental assessment covering the entire life cycle of a note—from printing to destruction.

The most practical path for India, therefore, is a phased experiment. A pilot project should begin with limited denominations and selected geographical areas. It should include humid cities, hilly regions, extremely hot zones, metropolitan markets and rural cash centres. During the pilot, an independent evaluation should be conducted of note life, counterfeit detection, ATM compatibility, public response, banking costs, recycling feasibility, and security impact. Only after such evidence has been gathered should any large-scale decision be made.

Polymer notes should neither be treated as a miracle nor dismissed as an unnecessary fashion. They can be a practical step towards improving the quality of cash management, provided they are introduced with economic prudence, technological preparation and public trust. In a country like India, currency is not merely a medium of payment; it is also a symbol of confidence. Any new banknote will succeed only if it is convenient in the pocket, acceptable in machines, economical for banks, difficult for criminals and trustworthy for citizens.

EXAGGERATED EXPECTATIONS

UNTIMATELY, the success of polymer notes will depend on whether the central bank views them merely as a change in material or as part of a broader currency reform. If the objective is durability, security, cost-efficiency and cleaner cash, considering polymer notes is reasonable. But if they are expected to deliver a decisive blow to black money, corruption and hawala networks, such expectations would be exaggerated. Whether a note is made of plastic or cotton-based paper, the real cleansing of an economy comes from policy, transparency and enforcement.

LETTER TO THE EDITOR FOR THE ISSUE DATED JULY 04, 2026

LETTER TO THE EDITOR FOR THE ISSUE DATED JULY 04, 2026 BATTLE WON BUT WAR REMAINS!

BATTLE WON BUT WAR REMAINS! BITCOIN FOR BEGINNERS! By Arvind Pinto

BITCOIN FOR BEGINNERS! By Arvind Pinto WHEN IT COMES TO BIRTHDAY CAKES I STILL WANT TO ORDER `BOL SANS RIVAL’…By Tara Narayan

WHEN IT COMES TO BIRTHDAY CAKES I STILL WANT TO ORDER `BOL SANS RIVAL’…By Tara Narayan GOA’S 56-VILLAGE U-TURN EXPOSES DEEPER CRISIS OF TRUST! By Dr Olav & Deborah Albuquerque

GOA’S 56-VILLAGE U-TURN EXPOSES DEEPER CRISIS OF TRUST! By Dr Olav & Deborah Albuquerque DEV BOREM KORUM… FOR SHARING MY JOURNEY OF 43 YEARS IN GOA!

DEV BOREM KORUM… FOR SHARING MY JOURNEY OF 43 YEARS IN GOA! FROM SOMNATH’S PLUNDER TO ‘CHANDA CHORI’ IN AYODHYA!By Ram Puniyani

FROM SOMNATH’S PLUNDER TO ‘CHANDA CHORI’ IN AYODHYA!By Ram Puniyani A SPOONFUL OF CAUTION: THE HIDDEN STORY BEHIND THE COMMON COUGH SYRUP! By Dr Amit Dias, MD

A SPOONFUL OF CAUTION: THE HIDDEN STORY BEHIND THE COMMON COUGH SYRUP! By Dr Amit Dias, MD WEEKEND UPDATESLETTER TO THE EDITOR FOR THE ISSUE DATED JUNE 27, 2026

WEEKEND UPDATESLETTER TO THE EDITOR FOR THE ISSUE DATED JUNE 27, 2026 ROMI KONKANI IS FLOURISHING: Nagri Konkani is sinking!

ROMI KONKANI IS FLOURISHING: Nagri Konkani is sinking! SCALPEL & SCAM: HOW INDIA’S HEALTHCARE CRISIS IS FUELLED BY GREED, GRAFT & GOVERNMENT APATHY! By Uday Barad

SCALPEL & SCAM: HOW INDIA’S HEALTHCARE CRISIS IS FUELLED BY GREED, GRAFT & GOVERNMENT APATHY! By Uday Barad INDIA’S GIG ECONOMY: GOA’S FLEXIBLE FUTURE OR FRAGILE REALITY? By Arvind Pinto

INDIA’S GIG ECONOMY: GOA’S FLEXIBLE FUTURE OR FRAGILE REALITY? By Arvind Pinto COME THE MONSOON SEASON AND EVERYONE WANTS TO FEAST ON FRYUMS!By Tara Narayan

COME THE MONSOON SEASON AND EVERYONE WANTS TO FEAST ON FRYUMS!By Tara Narayan MANAV-NAMA: REDISCOVERING THE ART OF BEING HUMAN! By Ranadhir Mukhopadhyay

MANAV-NAMA: REDISCOVERING THE ART OF BEING HUMAN! By Ranadhir Mukhopadhyay

Goa is abuzz with excitement as vintage bike and car owners, users, collectors and fans are decking […]